Fever-Tree: Solving U.S. Strategic Problem, Likely at the Right Price

Company Update (FEVR US) (Buy): U.S. beer giant Molson Coors will bring much-needed scale; we analyse the new agreement.

Highlights

Fever-Tree has given Molson Coors an exclusive U.S. license for royalties.

We believe this is the right answer strategically, and the terms seem fair.

Profits will take a hit in 2025, mostly from more U.S. marketing spend.

2024 sales showed an acceleration from H1, with 12% growth in the U.S.

At 775.0p, shares at 31x 2024 consensus EPS; we see large upside.

Introduction

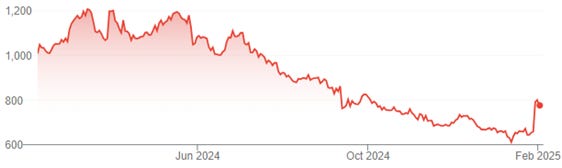

We review our Buy rating on Fever-Tree after it announced a new U.S. partnership with Molson Coors and provided a 2024 update last Thursday (January 30). Shares are 18% higher than before the news, but 23% lower than a year ago:

Fever-Tree Share Price (Last 1 Year)

Source: Google Finance (03-Feb-25).

We initiated our Buy rating on Fever-Tree in June 2024, and added it to our “Select 15” model portfolio as a small position in mid-July. Even after last week’s rally, Fever-Tree shares have lost 25% since our initiation (after dividends). We thought Fever-Tree shares were a Buy after they had fallen 60% since 2021 year-end, and we were still too early.

We believe the new partnership is a transformational step forward, will improve Fever-Tree’s financials significantly in the medium term and make a strategic sale even more likely. 2024 revenue figures confirmed momentum in the U.S.

(The rest of this article is for paid subscribers only, but unlocking it costs just $10; you can see a free sample of our research here.)