British American Tobacco: Fun While It Lasted? Looking Beyond Rally

Company Update (BATS LN) (Buy): Shares have fallen back after a multi-month rally, and structural concerns may be returning in H2

Highlights

The U.S. Tobacco earnings algorithm is broken for both BAT and Altria.

BAT needs a U.S. clampdown on vapes, which may not happen nationwide.

Timid buybacks and management reshuffles have added to our concerns.

We believe BAT needs a strong H2 to retain investor confidence.

With shares at 2,810.0 p, trailing P/E is 7.4x and Dividend Yield is 8.4%.

Introduction

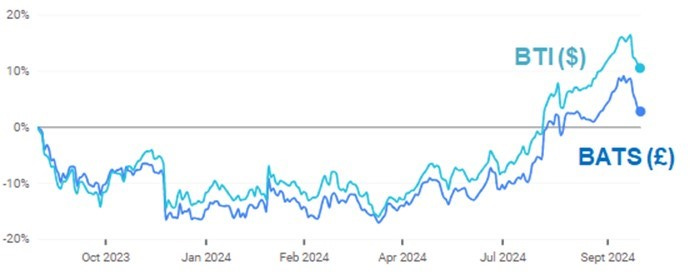

We review our Buy rating on British American Tobacco ("BAT") after the multi-month rally in its shares reversed, with its London-listed shares (“BATS”) falling back ~6% since their peak on September 11, and its American Depository Receipts (“BTI”) falling back by a similar ~5% from their peak on September 16:

BAT Share Price Performance (Last 1 Year)

NB. GBP/USD has risen by ~8% in the past year. Source: Google Finance (22-Sep-24).

BAT has been a small position in our “Select 15” model portfolio since September 2023, and we also hold BAT in real life. We have originally upgraded our rating on BAT to Buy in March 2020. BAT shares currently show a 17.9% gain in our model portfolio and a 49.7% gain since our initiation (in U.K. Pounds, including dividends). We last wrote about BAT in June, after its H1 2024 pre-close update.

We are increasingly uncomfortable with our BAT holding. Longstanding structural headwinds are persisting, and management’s ability to counter these seems no better than before. Retaining investor confidence will likely require H2 to show a material improvement. Valuation remains the only positive, with a 7.4x P/E and an 8.4% Dividend Yield.

(The rest of this article is for paid subscribers only, but unlocking it costs just $10; you can see a free sample of our research here.)