British American Tobacco: Leaking Bucket in H1, But ~10% Dividend Yield

Company Update (BATS LN) (Buy): More bad news as BAT reported its first H1 decline in revenue and profits since it acquired Reynolds in 2017.

Highlights

Both revenue and Adjusted Profit from Operations fell LSD in H1.

US combustibles industry volume fell ~9%; illicit Vapour grew again.

BAT continues to lose share in Heated Tobacco and Modern Oral.

P/E is 6.4x, FCF Yield is 15.5% and Dividend Yield is ~10%.

At 2,422.0 p, we see 76% total return (28.5% p.a.) by 2026YE. Buy

Introduction

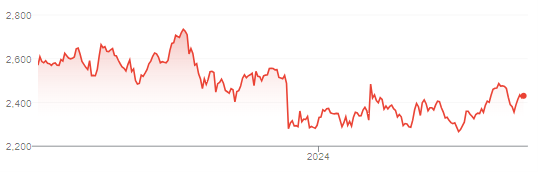

British American Tobacco ("BAT") provided a “pre-close update” for H1 2024 yesterday (June 4). BAT shares initially fell by 1.5%, before finishing the day down 0.5%, which means they are still down ~5% in the past year:

BAT Share Price Performance (Last 1 Year)

Source: Google Finance (05-Jun-24).

We have had a Buy rating on BAT since March 2020 and added it to our “Select 15” model portfolio last September. We also hold BAT in real life, but a far smaller position compared to Philip Morris (“PM”), which is a core holding.

With less than a month left in H1, the update provides good insight on likely BAT H1 results and is also the last reliable datapoint for PM and Altria before they report Q2 results in the last week of July.

BAT saw its first H1 decline since at least the Reynolds buyout in 2017, with both revenues and Adjusted Profit from Operations (“PfO”) falling by low-single-digits organically, albeit after a 2 ppt inventory impact in U.S. Combustibles.

For other Tobacco companies, we see BAT’s pre-close update as positive for Philip Moris (good cigarette trends outside the U.S., continuing PM dominance in New Categories), negative for Altria (continuing volume headwinds for U.S. cigarettes) and slightly negative for Imperial Brands (the U.S. being ~30% of its revenues).

(The rest of this article is for paid subscribers only, but unlocking it costs just $10, less than half the price of a single BAT share; you can see a free sample of our research here.)