Brown-Forman: 10% Bounce, Recovery Still to Come After Q3 FY25

Company Update (BF.B US) (Buy): 6% organic growth did not mean a recovery has begun, but seemed enough to force some shorts to cover.

Highlights

Organic net sales growth accelerated to +6% from +3% last quarter.

This benefited from inventory, but outlook implies +2% growth in Q4.

European tariffs on U.S. Whiskey represent the biggest near-term risk.

Shares are at 20x trailing P/E and have a 2.5% Dividend Yield.

At $35.78, we see a 53% total return (14.9% IRR) by Apr-28. Buy.

Introduction

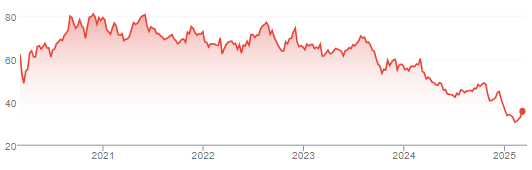

Brown-Forman released Q3 FY25 (November-January) results on Wednesday (March 5); shares finished up 10.1%, though falling back 0.6% the day after and, at $35.78, remain at less than half of their $80+ peak back in 2020:

Brown-Forman Class B Share Price (Last 5 Years)

Source: Google Finance (06-Mar-25).

Brown-Forman shares similarly jumped 10.7% after Q2 FY25 results on December 5, even though the results were less rosy than the headlines (as we pointed out at the time). These dramatic swings are likely the result of the high short interest in the stock, currently at ~27m shares (or ~9% of the total outstanding Class B shares).

(All references to Brown-Forman share prices here are based on the more liquid non-voting Class B shares.)

We upgraded our rating on Brown-Forman to Buy in June 2024 and added it to our “Select 15” model portfolio as a small position in the same month. Shares have lost 17.0% since our initiation (after dividends).

Q3 FY25 results show stability in the U.S. and European sales, and good Emerging Markets growth. While an actual market recovery is yet to materialize, the evidence continues to point to a cyclical downturn, not a structural decline.

(The rest of this article is for paid subscribers only, but unlocking it costs just $10; you can see a free sample of our research here.)