British American Tobacco: New FDA Ban on Vuse Alto Menthol Variants Means Little

Company Update (BATS LN) (Buy)

Highlights

Courts will put a stay on FDA bans and may overturn them

The key risk is still FDA’s plan to ban menthol cigarettes

Retention in previous menthol bans ranged from 65% to 110%

BAT would have a 10x P/E even if EPS is cut by 30%

At 2,444.0p, we see 115% total return (30.7% p.a.) by 2026YE

Introduction

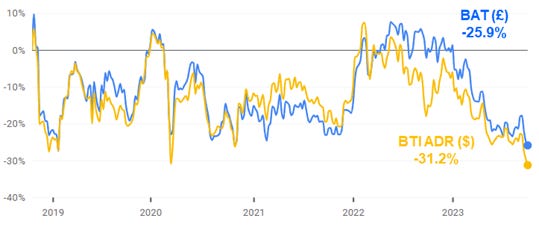

The FDA issued Marketing Denial Orders on 6 menthol and other flavour variants of Vuse Alto, British American Tobacco’s ("BAT") biggest Vapour product, on Thursday (October 12). BAT American Depository Receipts (“ADR”) fell by 4.8% in the subsequent 2 days, taking them to their lowest level since the COVID-19 trough in March 2020:

BAT Share Price Performance (Last 5 Years)

Source: Google Finance (13-Oct-23).

Excluding pandemic lows, the price of BAT’s ADR has not been this low since the 2008 Global Financial Crisis.

We believe the latest FDA bans were not a surprise and will be inconsequential. The FDA has consistently refused to authorize menthol and other flavoured Vapour products. BAT is…